Against the backdrop of a sweeping global carbon neutrality wave and the accelerated transformation of the global energy structure, Southeast Asia—with its robust economic growth vitality—has become a fiercely contested arena in the global green energy race. Situated at the core of Southeast Asia and guarding the golden shipping lane of the Malacca Strait, Malaysia has rapidly advanced into the central ranks of the Southeast Asian green new energy market. Blessed with unique natural resource endowments, clear national policy directions, and continuously climbing domestic electricity demand, the nation is attracting global capital and tech enterprises racing to establish their footprints.

Latest Hard Data! Malaysia's New Energy Enters an Explosive Cycle

The latest 2026 data released by the Ministry of Energy Transition and Water Transformation (PETRA) indicates that various core indicators have achieved leapfrog growth:

1. Renewable Energy Capacity: Target Adjusted Upward, Implementation Exceeds Expectations

As of December 2025, Malaysia’s renewable energy installed capacity accounted for 31% of its total energy mix, officially hitting the original 2025 target set by the National Energy Transition Roadmap (NETR). Deputy Prime Minister and Minister of Energy Transition and Water Transformation Fadillah Yusof explicitly stated that the government pledges to achieve a 32% renewable energy installation share in 2026, with plans to increase it by 1 percentage point annually, aiming to reach 35% by 2030 or even earlier.

According to the latest revised version of the NETR by the Malaysian government, the share of renewable energy installed capacity will sprint toward 40% by 2035, and reach 70% by 2050 alongside achieving carbon neutrality.

2. Solar PV Sector: Emerging from a Regional Low to Lead the Area in Annual Growth Rate

As the “main force” of Malaysia’s new energy, the solar photovoltaic (PV) industry has delivered the most brilliant performance. By the end of 2025, Malaysia’s cumulative installed solar PV capacity reached 5,777 MW (approximately 5.8 GW), with around 1,448 MW added throughout the year. Within this mix, the Large-Scale Solar (LSS) program contributed 2,648 MW, the Net Energy Metering (NEM) scheme contributed 2,747 MW, and the early Feed-in Tariff (FiT) program contributed 345 MW.

In the first half of 2025, newly added grid-connected solar PV capacity reached approximately 1.4 GW, with commercial and industrial (C&I) distributed solar accounting for over 60%. Factory rooftop solar retrofits have become a rigid demand.

Malaysia possesses superior solar resource endowments. The Peninsular Malaysia region sees an average annual sunshine duration exceeding 2,200 hours, while Sabah and Sarawak in East Malaysia exceed 2,500 hours. The cost of solar power generation continues to trend downward, with the current Levelized Cost of Electricity (LCOE) dropping as low as 0.18 MYR per kWh, demonstrating extreme market competitiveness.

Starting January 1, 2026, the “Solar Accelerated Transition Action Plan” (Solar ATAP) officially replaced the NEM scheme. It eliminated quota restrictions to drive the popularization of rooftop solar, but it strictly focuses on self-consumption and does not offer grid-feed revenue for excess electricity. The installation cap for residential users has been raised to 15 kW (three-phase), while the limit for commercial and industrial users stands at 1 MW or 100% of maximum demand.

3. Hydropower + Biomass: Traditional Advantage Sectors Continue to Deliver

Relying on the abundant river resources in East Malaysia, the nation’s hydropower installed capacity remains stable at 6.8 GW, accounting for 56% of total renewable energy installations and serving as the core anchor for baseload power.

Concurrently, as a major global producer of palm oil, Malaysia’s biomass energy potential has been thoroughly unlocked. According to the 2026 Budget, the government expects to roll out an additional 300 MW Feed-in Tariff (FiT) quota for biogas/biomass and small-scale hydropower. In 2025, biomass power generation capacity grew steadily. Utilizing agricultural wastes such as palm oil empty fruit bunches (EFB) and sugarcane bagasse to generate electricity not only resolves agricultural waste pollution but also achieves energy self-sufficiency, aligning perfectly with circular economy trends.

4. Green Electricity Demand: Industrial Drivers Widen the Supply Deficit

With data centers, semiconductors, and multinational manufacturing enterprises intensively clustering their operations in Malaysia, the demand for green electricity has experienced a meteoric surge. In 2024, power demand in Peninsular Malaysia hit a record 131 TWh, which is projected to grow to 135 TWh in 2025, representing an average annual growth rate of approximately 4.9% from 2025 to 2027.

The supply deficit for green electricity remains significant. The green power market size is expected to break past 800 billion MYR over the next 3 years, and this supply-demand gap translates directly into massive investment opportunities.

Policy Surge! Malaysia Invests Hundreds of Billions to Provide Reassurance

The explosion of Malaysia’s new energy sector is by no means accidental; it is driven by powerful top-down government enforcement. Policy dividends are landing intensively, creating what is considered one of the friendliest new energy business environments in Southeast Asia:

Maximized Tax Exemptions: New energy enterprises can enjoy a 10-year total corporate income tax exemption, zero customs duties on imported solar modules and wind power equipment, and a 100% Capital Allowance deduction for green power project investments. Furthermore, the Green Investment Tax Allowance (GITA) has been confirmed for extension through 2026, applicable to enterprises installing solar and energy storage systems.

Renewable Energy Fund Exemptions: Starting August 1, 2025, corporate consumers purchasing green electricity via the “Green Electricity Tariff” mechanism, cross-property power supply projects, or community cooperatives are exempt from contributing 1.6% to the Renewable Energy Fund (KWTBB). This lowers the procurement cost of green electricity by 5% to 10%.

Comprehensive Grid Upgrades: The government has allocated 43令吉 billion (43 billion MYR) to upgrade cross-regional grids across Peninsular and East Malaysia, directly addressing new energy integration challenges. Multiple core transmission lines completed capacity expansions in 2025, significantly elevating grid-connection efficiency for solar and hydro power.

Green Channel for Foreign Investment: Approval procedures have been simplified for Chinese new energy enterprises, drastically compressing the evaluation cycle for solar and energy storage projects. The government allows 100% foreign equity ownership in new energy projects, completely free from local equity binding requirements.

Energy Storage Implementations: In 2025, Malaysia’s first framework for large-scale shared energy storage power stations was deployed, with the government planning to reach 2 GW of storage capacity by 2030. The MyBEST initiative (400 MW/1,600 MWh) marks the beginning of Malaysia’s grid-scale energy storage deployment, which is expected to become fully operational by 2026/2027. Additionally, starting from 2026, self-consumption solar systems with a capacity exceeding 1 MWac are mandated to integrate a Battery Energy Storage System (BESS), accompanied by a standby capacity fee of 12 MYR per kW per month.

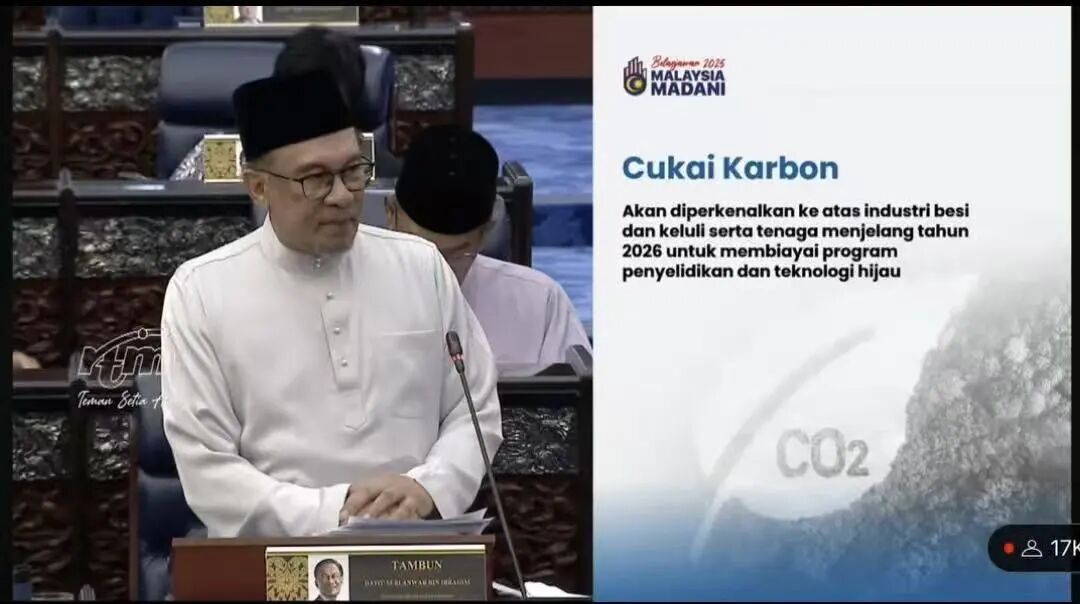

Carbon Tax Mechanism Initiated: Beginning in 2026, Malaysia will officially levy a carbon tax, initially targeting the iron & steel and energy sectors at an expected tax rate of approximately 15 MYR per ton of $CO_2$ equivalent, aiming to interface with the EU’s CBAM and indirectly stimulate renewable energy demand. However, in April 2026, the Minister of Natural Resources and Environmental Sustainability confirmed that due to geopolitical and energy cost pressures, the government has decided to temporarily defer the implementation of the carbon tax. Priority will instead be placed on establishing carbon credit and carbon market frameworks to avoid adding financial burdens onto industries and citizens.

Malaysia is a core member country of the ASEAN energy hub, and its new energy policies are deeply intertwined with the ASEAN Plan of Action for Energy Cooperation, allowing it to enjoy zero-tariff and market interoperability benefits within the ASEAN region. Furthermore, Malaysia is actively positioning itself as a central hub for cross-border electricity trading; the Lao PDR-Thailand-Malaysia-Singapore Power Integration Project (LTMS PIP) is already operational. Establishing a layout in Malaysia is equivalent to securing an “entry ticket” to the entire Southeast Asian new energy market.

A Golden Era of China-Malaysia Cooperation! Chinese New Energy Enterprises Emerge as the Biggest Winners

As the absolute leader of the global new energy industrial chain, China forms a perfect complement with Malaysia. The layout of Chinese enterprises in Malaysia’s new energy sector has experienced an explosive expansion across 2025 and 2026:

Solar Supply Chain Going Global: Top-tier enterprises such as JinkoSolar, LONGi, and Tongwei have established production bases for solar modules and cells in Malaysia.

Energy Storage & Technology Export: Companies like CATL and BYD have forged strategic partnerships with Malaysia’s national utility company, Tenaga Nasional Berhad (TNB), providing energy storage system solutions and smart grid technologies.

Opportunities for SMEs: Beyond the industry giants, a wave of Chinese supporting enterprises specializing in solar inverters, cables, and EV charging piles are entering the Malaysian market in bulk. In the first half of 2025, China’s export value of new energy equipment to Malaysia witnessed a significant year-on-year increase.

For independent entrepreneurs and industry practitioners, Malaysia’s new energy market also conceals quite a few “small yet beautiful” opportunities. For instance, commercial and industrial solar installation services, green power trading brokerages, new energy operation and maintenance (O&M) services, and cross-border equipment trade feature low barriers to entry but robust demand, making them excellent entry points into Southeast Asia’s new energy track.

Balanced Reflection Under the Trend! Pitfalls to Avoid Behind the Opportunities

Although the prospects for Malaysia’s new energy market are highly promising, the industry’s development still faces some realistic challenges. Entering enterprises must make preparatory adjustments in advance:

The Regional Disparity Trap: Peninsular Malaysia features comprehensive infrastructure and a mature market, making it suitable for anchoring commercial and industrial solar and energy storage. Conversely, East Malaysia boasts rich resources but weaker infrastructure, rendering it better suited for large-scale hydropower and utility-scale ground-mounted solar plants. Thus, when selecting regions, avoid blindly deploying a uniform layout across the entire nation.

Shortages in High-End Technology and Talent: The local market lacks adequate reserves in cutting-edge technological areas such as energy storage system integration, green hydrogen production, and smart grids. Concurrently, there is a shortage of specialized high-end talent in new energy R&D, project O&M, and technical commissioning, which limits the industry’s high-end upgrading. It is recommended to co-build R&D centers with local universities (such as the University of Malaya or UTM) to satisfy technology transfer requirements while cultivating local talent.

Certain Execution Barriers for Project Landing: Some large-scale new energy projects face complex land ownership situations, which can involve indigenous land rights and ecological protection issues. Furthermore, specific sub-sectors still maintain certain requirements regarding foreign equity limits and local employment ratios. Project environmental impact assessments (EIAs) and cross-departmental approval workflows can be time-consuming, requiring entering entities to prepare for long-term execution timelines to avoid affecting project realization efficiency.

Coexistence of Regional Competition and Profitability Pressures: Other ASEAN nations such as Vietnam, Thailand, and Indonesia are also stepping up their investments in the new energy sector, leading to increasingly fierce competition in the regional market. Fluctuations in global new energy equipment prices, combined with domestic electricity price regulations, compress project profit margins to a certain degree, placing higher demands on an enterprise’s cost control capabilities.

Conclusion: For Southeast Asian New Energy, Look to Malaysia for the Next Decade

Judging from the latest data, Malaysia’s new energy sector has officially transitioned from a “policy-driven” phase into a “market explosion” phase. With cumulative installed solar capacity breaking past 5.8 GW, the renewable energy share hitting 31%, the energy storage market fully activated, the carbon tax mechanism anchored, and the successful convening of the China-Malaysia Cooperation Roundtable—doubled installations, skyrocketing demand, and policy safeguards, combined with the golden era of China-Malaysia relations, are turning this into the most predictable new energy boom in Southeast Asia.

Whether for leading enterprises establishing global manufacturing capacity, SMEs mining specialized niche tracks, or independent individuals seeking cross-border entrepreneurial opportunities, Malaysia’s green new energy track is highly deserving of focused attention.

The global trend toward carbon neutrality is irreversible, and Southeast Asia’s energy transition is already on the launchpad. Malaysia is precisely that undervalued golden destination. Capturing this wave of dividends could mean seizing the premium new energy opportunities for the next decade!